Speculating on a Distressed Special Situation

Ashford Hospitality Trust (AHT): $2.6 billion of non-recourse debt, a huge advisor termination fee with priority claim, and a stub that’s worth somewhere between zero and several times today's price.

Every so often a stock turns up on the distressed pile looking like an obvious mispricing, and the interesting part of the work is figuring out whether it actually is one or whether the market has already priced something I haven’t found yet. Ashford Hospitality Trust (NYSE: AHT) is the second kind. At around $3 a share ($3.22 as of the 6/22/26 close), sitting on a portfolio of hotels that on a decent day appraise for more than the mortgages against them, the common looks like a cheap call option on a hotel recovery. The catch, and with these situations there’s always a catch, is that AHT doesn’t fully control its path to value realization (mostly a sale or liquidation). It is run by an external advisor, Ashford Inc., which holds a contractual termination fee that ranks senior to every other claim in the capital structure, and that fee is large enough to absorb most or all of whatever the common might otherwise collect in a sale.

Once I put that fee where it sits in the waterfall, the stock stops being a cheap option on the assets and becomes a thin, binary residual: potentially worth nothing, potentially worth a few times today’s price, with very little ground in between. I want to be clear that this is a speculative situation with a genuine path to zero for the common. This isn’t an investment I’d sink my kids’ college funds into. But I’m writing it up because the way the pieces fit together makes it unusual and I think it’s been left for dead (maybe rightfully so). This is anything but a layup.

A quick snapshot before the walk-through:

Price: $3.22 as of today’s close (June 22, 2026)

Shares outstanding: ~6.5 million (after two reverse splits…)

Market cap: ~$20 million (very thinly traded, often less than 50k/day)

Total debt: ~$2.6 billion, roughly 94% floating, ~7.9% blended rate

Preferred: 9 series, ~$372 million liquidation preference, dividends suspended

Portfolio: ~60 hotels, ~15,000 rooms, upper-upscale full-service

External advisor: Ashford Inc. (I wouldn’t let these guys advise my worst enemies)

The business

AHT owns hotels. It doesn’t run them and it doesn’t really manage itself either. The properties are operated by third-party managers (a large share by an Ashford affiliate), and the company as a whole is steered by Ashford Inc. under a long-term advisory agreement. AHT pays Ashford a base advisory fee scaled to its total market capitalization, reimburses a pile of costs, and the broader Ashford complex collects additional fees for hotel management, project management, debt placement, and insurance. That external structure is not a side note. It is arguably the single most important feature of the investment (right alongside the hotel portfolio cap rate estimate), and it’s why a pile of hotels that could be worth more than their mortgages does not translate cleanly into value for the people who own the common shares.

The underlying business is what you’d expect: revenue per available room drives the top line, the assets consume capital with maintenance and upgrades, and the whole thing fluctuates with the travel cycle and with interest rates. None of that is unusual for a hotel REIT. What makes AHT its own animal is how much debt it carried into a bad stretch and who stands where when the proceeds get divided up.

How it got here

The short version is that AHT went into the pandemic over-levered and spent the years since digging out, on terms that mostly favored everyone except the common. COVID gutted hotel cash flow, the company took expensive rescue financing to survive (including a term loan it later repaid with a sizable exit fee), and it leaned on its own broker-dealer to sell a large block of non-traded preferred stock to raise capital. Along the way it ran preferred-for-common exchanges that an activist holder publicly called self-dealing, suspended the common dividend, and did two reverse splits to hang onto its listing.

More recently the playbook has been divestment: sell hotels, mostly at 6% to 7% cap rates, and use the proceeds to pay down mortgage debt. The portfolio has shrunk from around 100 hotels to roughly 60. The problem is that about 94% of the remaining debt floats, so as rates climbed the interest bill swelled even as the asset base got smaller, and the math at the equity line kept getting worse. The company suspended its preferred dividend in January 2026. First-quarter 2026 brought a net loss, a $113 million impairment across nine hotels, a stockholders’ equity deficit of roughly $695 million, and a going-concern warning that pointed at about $1.9 billion of non-recourse loans maturing within a year. After interest, the equity has been burning cash, with the FY2025 Adjusted FFO at negative $34 million.

The Braemar situation

Here’s where it gets even worse, and where I’d point anyone trying to understand the governance. It’s also why I’m not mincing words when it comes to my description of the external advisor relationship. It’s bad. They might as well be the advisor from hell.

Ashford Inc. advises a sister hotel REIT, Braemar Hotels & Resorts (BHR), under the same kind of agreement. In 2025 Braemar put itself up for sale. The fee to exit the Ashford advisory relationship in a change of control was calculated (by Ashford Inc. and BHR) at a “fair and reasonable” $574.83 million, then negotiated down to a $480 million company sale fee. For reference, BHR operates a platform smaller than AHT. The advisor collected a $17 million advance on signing and stood to receive another $25 million if a buyer wanted out of the affiliated management and project agreements.

Just recently, Braemar’s board looked at the math and concluded that a sale wasn’t the value-maximizing path, largely because that fee skims proceeds off the top before public shareholders see anything. Instead, they decided to terminate the advisor and internalize management while staying public. A pretty remarkable outcome. A company with willing buyers in the asset market chose not to sell because the cost of leaving its advisor was too high relative to what shareholders would keep.

AHT has the same advisor, the same fee mechanism, and an agreement that AHT amended in March 2026 to make the structure even stickier. The advisory term was pushed out to 2055, the termination fee was defined as thirty years of foregone advisor earnings discounted at 2% (which works out to a multiple of roughly 22 times), and AHT gave up its ability to terminate. The advisor also has access to the company’s bank accounts and the contractual ability to escrow the fee. I’m not in the business of guessing intentions, and I’d rather let the structure speak, but it is hard to look at this arrangement and conclude that the incentives point at the AHT common holder.

(You can read what BHR’s largest shareholder had to say about Ashford Inc.’s termination fee here: Al Shams Investments Responds to Braemar Board's Brazen Act of Self-Dealing)

The debt

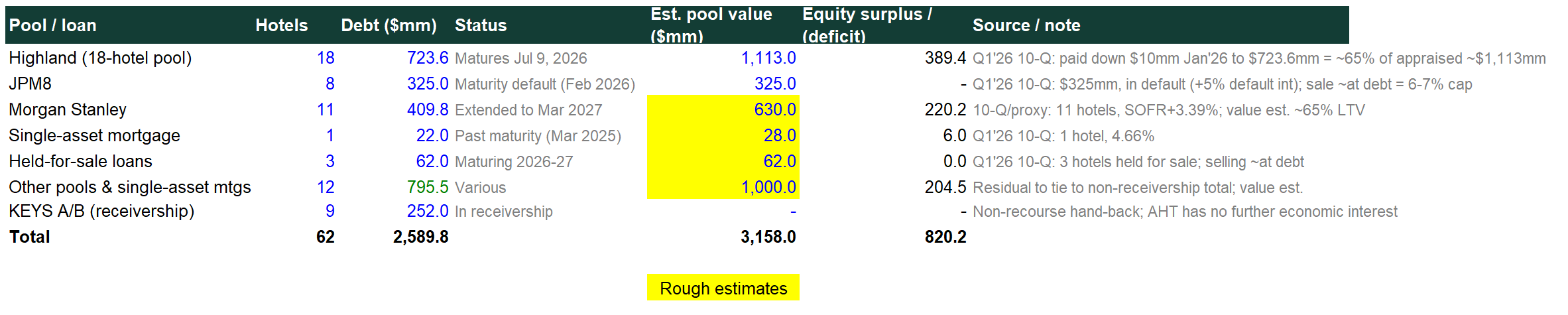

The mortgage stack is about $2.6 billion all-in, all of it non-recourse, and most of it floating. The pieces worth highlighting:

Highland: 18 hotels, about $724 million, matures July 2026. The loan was paid down $10 million in January to roughly 65% of appraised value, which backs into a collateral appraisal around $1.1 billion. This is the pool with real equity cushion.

JPM8: 8 hotels, $325 million, already in maturity default with default interest piling on top of the stated rate.

Morgan Stanley: 11 hotels, about $410 million, extended out to March 2027.

KEYS A/B: 9 hotels, roughly $252 million, already in receivership and effectively gone.

The non-recourse feature cuts both ways. It caps the damage from any single underwater pool, because AHT can hand the keys back rather than write a check (which is exactly what happened with the KEYS hotels). But it also turns the near-term maturity wall into a string of refinance-or-surrender decisions, and at something like 8% money against hotels, a few of those pools simply won’t survive. The handful that carry obvious equity, Highland chief among them, are the ones that actually matter to a recovery case.

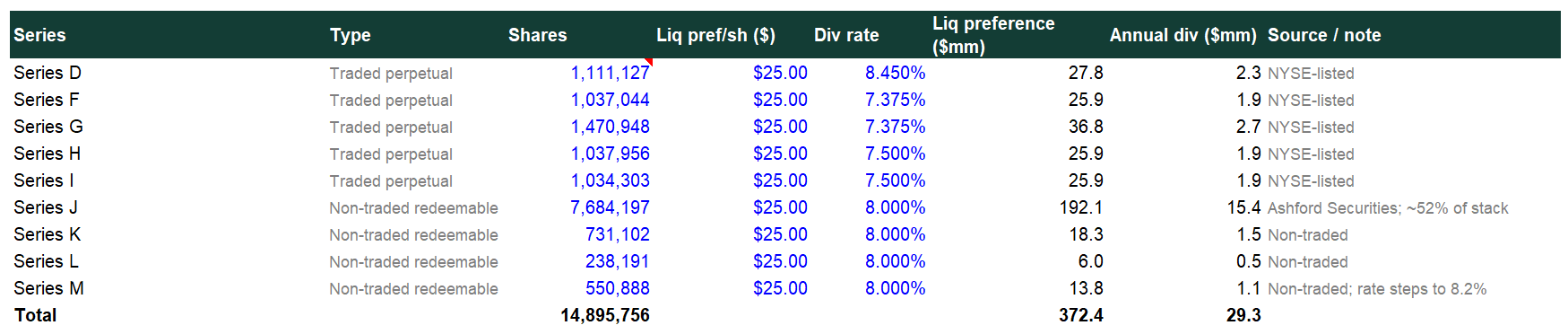

The preferred

There are nine series of preferred, with a combined liquidation preference of about $372 million at $25 a share. The dividends are suspended and accruing. In a liquidation or change of control these are fixed cash claims that sit ahead of the common, and the large non-traded series (the ones sold through Ashford’s own broker-dealer) redeem in cash with no conversion into stock. The primary offering of those non-traded series was shut down at the end of 2025, so the roughly $372 million is effectively close to a ceiling on this claim that climbs only with the more time the preferred dividends are suspended and they accrue in arrears (~$30 million per year).

The preferred pricing here is pretty telling. The listed Series D trades around $9, roughly 36% of its $25 par. So the market expects the preferred to be impaired, despite a recent “independent” appraisal suggesting otherwise. Since the preferred obviously ranks above the common, that data point speaks volumes about why the common trades where it does

The advisor fee and the wind-down

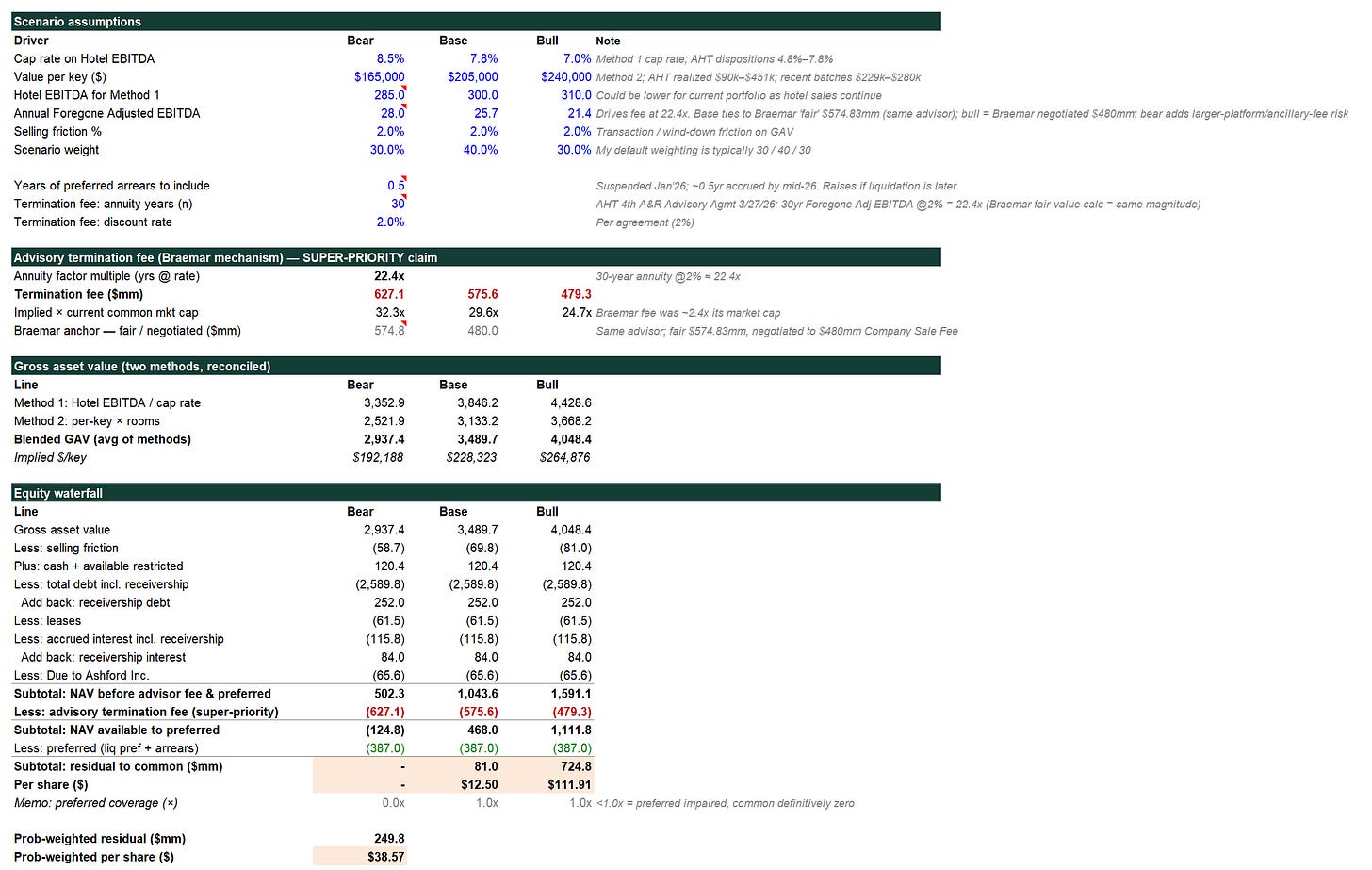

On a change of control, the advisor’s termination fee is paid out of net proceeds first, ahead of both preferred and common. Using AHT’s own formula (about 22 times foregone advisor earnings) and anchoring to the Braemar fair-value figure on a comparable platform, I peg the fee at roughly $575 million in the base case, inside a range of about $480 million (the Braemar negotiated number) to $630 million (allowing for AHT being a larger platform, and for the kind of ancillary-fee inflation a Braemar activist complained about). On top of that there’s about $66 million already owed to Ashford on the balance sheet.

It’s worth pinning down what actually trips that change of control, because it isn’t only a sale of the whole company. The agreement also counts asset sales. Dispose of 20% of the company’s assets by book value in any one-year period, or 30% over any three years, and a change of control is deemed to have occurred. Sales to Braemar are excluded, and the ordinary one-off dispositions get kept under that line on purpose. The small Jacksonville hotel the company sold in June for about $11 million is exactly that sort of sale, and it does nothing to the fee. What matters is the two troubled loan pools. Highland and JPM8 are carved out of the calculation only through November 15, 2026, and after that date, if the lenders take those hotels back, the handbacks begin to count toward the threshold. That timing is why the company’s own going-concern language names November 16, 2026 as the date the fee could begin to be triggered. There’s a cash-flow test bolted on as well, where the advisor can pull the trigger only if the portfolio’s annualized cash flow after debt service sits below $65 million, but AHT is already well under that figure, so the test reads as satisfied rather than protective. Put the pieces together and the catalyst isn’t the steady drip of small sales. It’s the forced surrender of Highland or JPM8 once the carve-out lapses this November, or a sale of the whole company, and either route pays the advisor first.

Stack it up and you have something north of $900 million of claims (the super-priority fee plus the preferred) that has to be satisfied before the common collects a dollar, against a portfolio whose equity value above the mortgages lands in roughly that same neighborhood. That is the entire ballgame. The fee isn’t a rounding error against the equity, it’s comparable in size to the equity, and it gets paid first. Unbelievable.

So what’s the common actually worth

Running the waterfall estimate creates the shape of the bet. Value the hotels across a range of cap rates and per-key prices consistent with AHT’s own recent sales (call it 7% to 8.5% caps and $165k to $240k a key), subtract the debt, the leases, the accrued interest, and the money owed to Ashford, then take out the super-priority fee, then the preferred, and whatever survives is the common.

Bear: zero. The fee alone exceeds what’s left after the mortgages, so the preferred and the common are both wiped.

Base: roughly $13 a share.

Bull: roughly $112 a share. (this is incredibly unlikely; waterfall mechanics are highly sensitive to the range of inputs due to leverage impact on residual value)

Probability-weighted: high-$30s (I used my standard 30/40/30 bear/base/bull weighting here as a default; if I assume a 50/40/10 weighting to risk more to the zero case, the probability-weighted value drops to ~$16)

Now the part that keeps me honest. At ~$3, the market is implying a portfolio value right around where the base case breaks even, an implied cap rate near 8.7% on the hotels, which is a notch worse than where AHT has actually been transacting. The current price is not obviously wrong. It is pricing the common as a sliver of option value sitting right at the knife’s edge where the assets, the fee, and the preferred net to about zero. Push cap rates down toward where the better hotels trade and the common is worth a multiple of today’s quote. Push them up, or let the fee land at the high end, and it’s a donut. The value isn’t smeared across a range so much as it sits on a switch. Another way to look at it using my probability weighting approach is solving for a probability of zero common value by goal-seeking to a percentage that matches the current market price (with no weighting to an upside case). Doing so backs into the market pricing a 75% chance of zero equity value and a 25% chance of my base case value.

Option value

I’ll say plainly what this is: a speculation, not an investment with a margin of safety underneath it. The downside is a real zero, not a figure of speech, and the going-concern language and the maturity wall mean that zero isn’t a remote tail. The reason it’s interesting at all is the asymmetry. The dollars at risk per share are small, the upside if the hotels clear at strong caps and the fee lands at the negotiated end is a genuine multiple, and the things that decide which way it breaks are few and identifiable rather than a fog of unknowables.

The swing factors come down to the cap rate the portfolio ultimately fetches, the size of the fee the advisor actually extracts, and whether the near-term mortgages get refinanced or handed back. Get a feel for those three and you’ve got the whole position. For folks who are willing to size a speculative idea small and watch it play out, AHT is worth understanding and following. I wouldn’t fault anyone for passing on it on governance grounds alone, and I’d fault no one for treating any position as money they’re prepared to lose.

DISCLOSURE: I own AHT at around a $3.10 cost basis

I write Bedrock Value as an individual investor sharing my own research and opinions. I am not a registered investment adviser, a broker-dealer, or a personal financial professional of any kind, and nothing in this piece is investment advice or a recommendation to buy, sell, or hold any security. It is published for informational and educational purposes only.

This is a speculative situation. As I say in the body, the common stock has a real and plausible path to zero, and you should treat any capital put into a name like this as money you are fully prepared to lose. Distressed equities, thinly traded small-caps, and companies operating under going-concern warnings carry risks well beyond those of ordinary stocks, up to and including total loss. This particular situation ticks all three of those important boxes.

Do your own work. Read the filings yourself, reach your own conclusions, and if you want advice tailored to your circumstances, please consult a licensed financial adviser (which, again, I am not).